Let me explain a little bit about this MERS problem...

Unless you have three kids under the age of 4, watch only the Sprout channel and have no time to read the paper, you have heard about the foreclosure paperwork mess (otherwise known as FRAUD).

An acronym being tossed around in these reports, MERS, is a (pseudo) company at the center of one of the main issues

MORTGAGE ELECTRONIC REGISTRATION SYSTEMS INC...the actual name of the business entity. MERS is a Delaware corporation whose sole shareholder is Mers Corp. MersCorp and its specified members (the Lending Institutions) have agreed to include the MERS corporate name on any mortgage that was executed in conjunction with any mortgage loan made by any member of MersCorp. (UPDATE 9/1/2010: 65 MILLION American Mortgages).

MERS is a shell corporation with no employees, but thousands of officers

In the mid-1990s mortgage bankers decided they did not want to pay recording fees for assigning mortgages anymore. This decision was driven by securitization—a process of pooling many mortgages into a trust and selling income from the trust to investors on Wall Street. Securitization, also sometimes called structured finance, usually required several successive mortgage assignments to different companies. To avoid paying county recording fees, mortgage bankers formed a plan to create one shell company that would pretend to own all the mortgages in the country—that way, the mortgage bankers would never have to record assignments since the same company would always “own” all the mortgages.

From the site StopForeclosureFraud.com comes the following: Thus in place of the original lender being named as the mortgagee on the mortgage that is supposed to secure their loan,MERS is named as the “nominee” for the lender who actually loaned the money to the borrower. In other words MERS is really nothing more than a name that is used on the mortgage instrument in place of the actual lender. MERS’ primary function, therefore, is to act as a document custodian.

MERS was created solely to simplify the process of transferring mortgages by avoiding the need to re-record liens – and pay county recorder filing fees – each time a loan is assigned. Instead, servicer’s record loans only once and MERS’ electronic system monitors transfers and facilitates the trading of notes. It has very conservatively estimated that as of February, 2010, over half of all new residential mortgage loans in the United States are registered with MERS and recorded in county recording offices in MERS’ name.

MersCorp was created in the early 1990’s by the former C.E.O.’s of Fannie Mae, Freddie Mac, Indy Mac, Countrywide, Stewart Title Insurance and the American Land Title Association. The executives of these companies lined their pockets with billions of dollars of unearned bonuses and free stock by creating so-called mortgage backed securities using bogus mortgage loans to unqualified borrowers thereby creating a huge false demand for residential homes and thereby falsely inflating the value of those homes...

The MERS paperless system is the type of crooked rip-off scheme that is has been seen for generations past in the crooked financial world. In this present case, MERS was created in the boardrooms of the most powerful and controlling members of the American financial institutions. This gigantic scheme completely ignored long standing law of commerce relating to mortgage lending and did so for its own personal gain.

The American media routinely identifies MERS as a mortgage lender, creditor, and mortgage company, when in point of fact MERS has never loaned so much as a dollar to anyone, is not a creditor and is not a mortgage company. MERS is merely a name that is printed on mortgages, purporting to give MERS some sort of legal status, in the matter of a loan made by a completely different and almost always,a totally unknown entity.

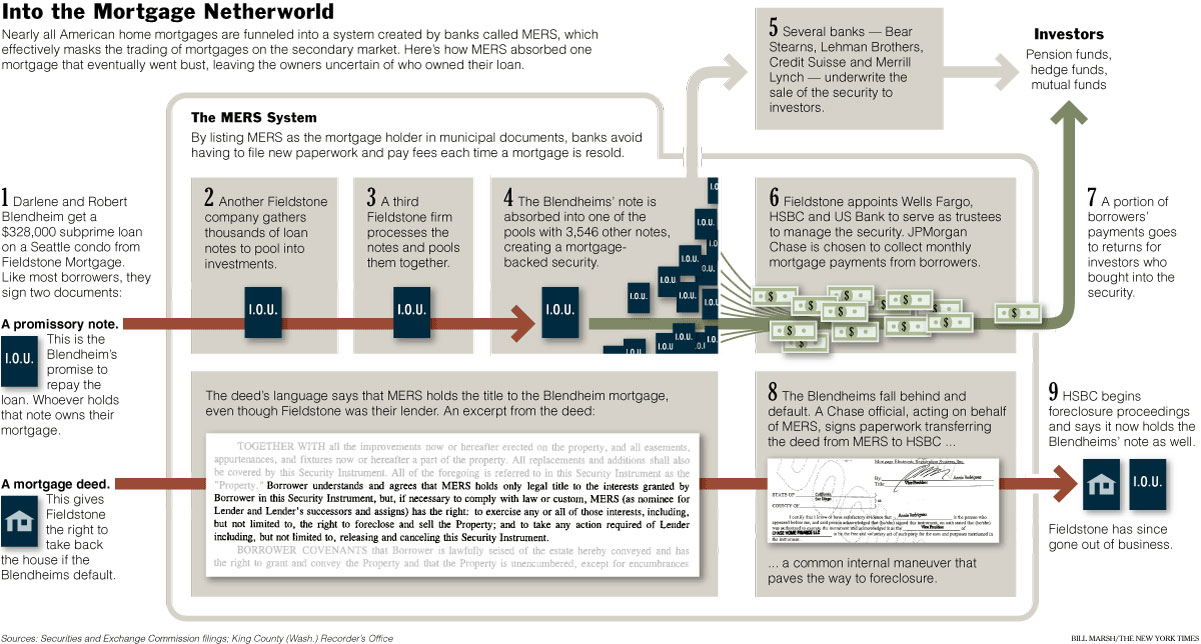

Here is a graphic that concisely explains the scam...er, I mean process:

Now here is the big SCAM component of MERS (taken from a Law Review paper written by Professor Christopher Lewis Peterson, Univ of Utah): To accommodate the massive amount of paperwork and litigation involved with its business model, MERSCORP simply farms out the MERS, Inc. identity to employees of mortgage servicers, originators, debt collectors, and foreclosure law firms...MERS invites financial companies to enter names of their own employees into a MERS webpage which then automatically regurgitates boilerplate “corporate resolutions” that purport to name the employees of other companies as “certifying officers” of MERS. These certifying officers also take job titles from MERS stylizing themselves as either assistant secretaries or vice presidents of the MERS, rather than the company that actually employs them. These employees of the servicers, debt collectors, and law firms sign documents pretending to be vice presidents or assistant secretaries of MERS, Inc. even though neither MERSCORP, Inc. nor MERS, Inc. pays any compensation or provides benefits to them. Astonishingly, MERS “vice presidents” are simply paralegals, customer service representatives, and foreclosure attorneys employed by other companies. MERS even sells its corporate seal to non-employees on its internet web page for $25.00 each. Ironically, MERS, Inc.—a company that pretends to own 60% of the nation’s residential mortgages—does not have any of its own employees but still purports to have “thousands” of assistant secretaries and vice presidents...

I won't go into any further sordid details here, as you'd probably fall asleep. But I wanted to start this series of posts with this brief explanation of one of the main players in the "Foreclosures Gone Wild" game. Stay tuned for ...the rest of the story.