If you would like to set up a private, early, viewing please email me here

Thank you for reading!

Steve & Jackie Jackson

And the Jackson Realty Group

Please call me at 561.602.1258 if you know someone who may be interested in this unique home!

Steve Jackson

Move-in condition, 4 bedroom Nairobi model on one of the biggest lots in Winston Trails!

A yard like this is a rarity in Winston Trails. You may not have the opportunity to get a lot like this for years! Biggest lot available in Winston Trails! Real estate value is primarily about location and this one is great! Private cul-de-sac spot...Big roofed and screened patio maximizes your enjoyment of this wonderful yard...one side of your back yard fronts a canal and the other fronts a park-area/playground. New A/C, Tile and laminate flooring...Accordion shutters...move-in condition. Asking price: $335k

Call me directly for a private viewing: 561.602.1258

Thanks for reading…Steve Jackson, The Jackson Group

If you think your home should be marketed like this…please give me a call at 561.602.1258

or email me at email link

Thanks..Steve Jackson

Unbelievable! This unfortunate seller…they thought they’d be smart and save money on commissions by hiring a gimmick company. But boy…did they end up paying.

A properly consulted, marketed, represented, and negotiated Winston Trails home sale will be at about 96-97% of asking, this poor home seller got less than 86% of what they were planning on!

There is a reason we have sold almost 500 Winston Trails homes, have been selling in here since the construction trailer was up, and continue to get referrals from past Winston Trails clients. Meet with us if you’re thinking of selling…there really is no substitute for the extensive experience we have.

Thanks for reading!

Steve Jackson

561 602 1258

From the insightful Dr. Housing Bubble blog:

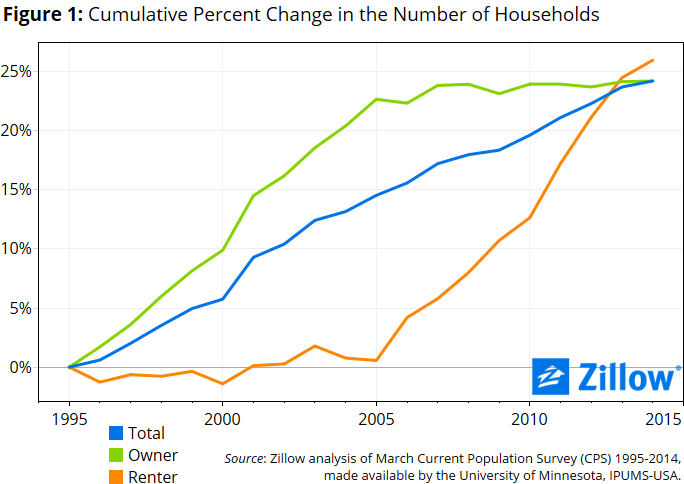

What a difference a decade can make. Over the last two decades the number of U.S. households has grown by 25 percent. But the growth has come in two distinctive waves. Between 1995 and 2005 nearly all of this growth came in the form of new homeowners. However, the subsequent decade saw something very different. Most of household growth between 2005 and 2015 has come in the form of renter households. It should come as no surprise that new home buying still remains weak. With this new trend unfolding, it shouldn’t come as a shock that multi-unit permits are surging as builders place their bets on rental Armageddon. While a few people can’t wait to dive into mega debt for a crap shack, others are simply renting either out of necessity or by choice. In fact, renting over the last decade has been the choice many have made (out of necessity or free will) contrary to the crap shack enthusiasts trying to talk up their poorly built piece of junk as some kind of diamond in the rough. Builders with deep pockets are betting on a continuation of the rental trend. It should also be no surprise that this decade saw a major surge of the “single family home” as rental unit.

Two decades with two different stories

We have witnessed continued household growth in the U.S. Household formation has increased by 25 percent over the last 20 years. However, each half of the last 20 years has seen growth come from two very distinct categories.

The homeownership boom followed by the renter boom:

The chart above is as clear as day. You have the last hurrah leading to peak homeownership followed by a massive shift to renting as millions upon millions of Americans lost their homes to foreclosure. You need to remember what this has done to consumer psychology. Never in our lifetime have we witnessed a countrywide housing bubble. Housing before this recent crash never suffered one year of negative price growth. Not one. So this put a major dent into the untouchable perception of housing as a sure bet. It also didn’t help that over 7 million Americans actually lost their home to foreclosure. We now have a nice group of revisionists talking about these people “strategically walking away” but in reality, this was a small subset. The majority lost their home because when the economy contracted, cut wages and lost jobs couldn’t cover the mortgage payment. Research has shown that people will prioritize debt payments in crisis and housing gets pushed up to the top of importance. So losing a home is a big deal and certainly most people lost it for this obvious reason. But you have to live somewhere. Where did these people go?

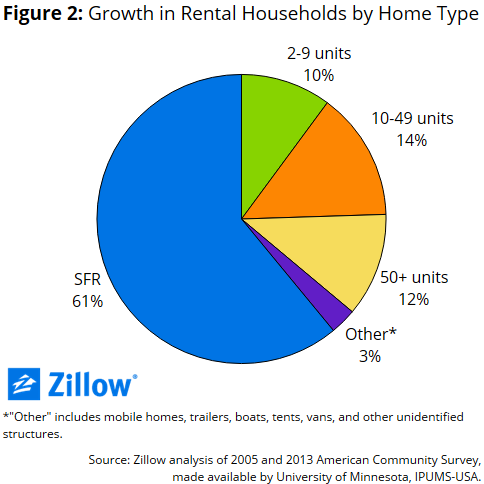

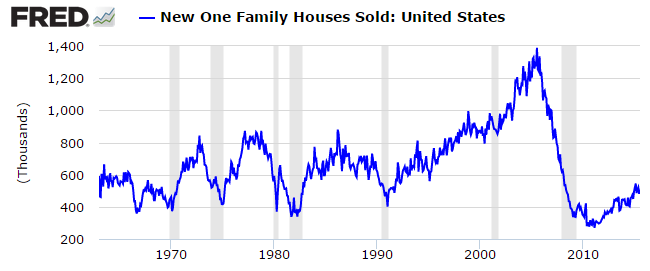

A large part of the single family home inventory got sucked up in the investor orgy to convert them into rentals. This took an already low supply of homes and made it lower. And builders simply did not build new homes in large quantities because new home sales continue to be pathetic:

Why not build new homes if supply is so low? The answer is clear and that is new potential households have weaker wages and new homes cost more. Why would builders construct an expensive product when the demand based on household income is for rentals? It is also the case that younger households watching mom and dad stressing their minds our to make the mortgage payment has left an indelible memory on their mind. Homeownership isn’t all that it is cracked up to be. Millennials certainly don’t have the taste for home buying like the Taco Tuesday baby boomer generation…People simply can’t afford to buy even with the Fed holding rates near zero.

19 homes!

Excluding foreclosures, there are only 19 homes on the market in Winston Trails today…and only 1 larger than 2400 sq. ft.! (there are 4 distressed sales). That is out of more than 1800 homes. Inventory has not been this low in quite a while.

If you have one of the larger homes in Winston Trails and are thinking about selling…now may be a good time. Typically the buyer traffic slows down after school starts, but there are always buyers interested in purchasing a home in our community. We are blessed to be in A rated school districts from elementary through high school…that continues to makes our community desirable to the family demographic.

We had a very good summer in here, with prices maintaining their gains and days on market falling. Since the beginning of our community, the variations in sales activity have been extremely predictable…but even with a bit of a slower time ahead of us, the low inventory, especially of the larger homes, bodes well for sellers.

Thanks for reading!

And give me a call or send me an email with any questions about our market in Winston Trails.

Steve Jackson

561.602.1258

Your Neighborhood REMAX…Right across the street next to Winn Dixie

Winston Trails Homeowners,

There is a Winston Trails Foundation, Inc. Board of Director Meeting scheduled for Thursday, August 13, 2015 at 7PM. The meeting will be held at the Swim & Racquet Center. The agenda will include approval of the seal coat proposals for 2015, Channel 63, and possibly approval of the repair work for the pool at the Swim & Racquet Center. Sign-In will start at 6:30 PM and homeowners may be required to show photo identification. All homeowners are welcome and encouraged to attend.

According to the FBI, property and mortgage/property fraud is the fastest growing white-collar crime in the US.

Criminals file fake deeds making it appear that they own homes they actually have no ownership interest in. They can then defraud potential tenants or buyers out of money by renting out the house they don’t own or actually selling a house they don’t own!

Below I have included a link that gives you the ability to receive notification should anyone file/record a document in Palm Beach County using your name (or your business name). This is a free service!

Keeping an eye on your property records is one important way to protect yourself from fraud.

Thanks for reading my blog.

Steve Jackson, REMAX 360

561 602 1258

I live in Winston Trails and I get a real estate postcard from this one agent at a rate of about 1/week! Owners see that and must think…”she must be good”…and can then end up like the poor sellers below who will wonder why nobody is looking at their beautiful Winston Trails POOL home.

When a buyer or agent does a search for a pool home in Winston Trails…this will be invisible.

I have found that when an agent has a ‘big team’, things like this happen and fall through the cracks. The ‘big team’ agents sometimes won’t even come out to the initial appointment, instead sending a “specialist’ (what make them a specialist?), they tend to be ‘numbers driven’, not customer service driven, passing off almost all communications and processes to newbies. I have heard of one agent who does not even give clients her cell phone number!

Just be careful who you hire to sell your home…what you don’t know can hurt you badly.

Thanks for reading my blog!

Steve Jackson

561 602 1258

A pristine, move-in-condition, Paris model on a big, interior lot will be coming to the market in the next week. It is a true 5 bedroom (not the model with a loft), granite, stainless…It will be offered at $350,000.

There is a great deal of competition this time of year for the larger homes…so if you or someone you know has an interest in this type of home in Winston Trails, have them call me at 561 602 1258 and get the opportunity to see this home before it hits the MLS.

Dear Fellow Presidents, Board Members, and Residents

You all know me as the Comcast guy. I am the Regional Manager for Comcast Bulk Services in Palm Beach County. I am also a long term resident of WT (17 years) and have the privilege of serving Bermuda Dunes Village as its Association President. I do my best to attend all Foundation meetings and contribute, as needed, in a positive and professional manner.

Upon receiving and reading the Foundation letter sent to residents this week about our bulk cable services, I am shocked and dismayed by the false and misguided statements made about Comcast's technical capabilities (Coaxial vs. Fiber Optics) and the proposal to WT to continue to be the provider of choice for our residents. It is now clear that the "Cable Committee", consisting of just two members..Brad Bastien and Guy Buzelli, have unilaterally decided on the merits of Hotwire's offering WITHOUT allowing Comcast to respond with its own competitive value proposition. It appears that the "Committee", was motivated from the beginning of the negotiations to "get rid of Comcast". They did not negotiate in good faith and filtered information to the board that led them to agreeing to switch to Hotwire.

Getting the facts straight:

The section of the Foundation letter comparing Coax Cable and Fiber Optic is wrought with mis-information and lacks any level of credible technical claims. It's obvious the statements made (see below) are written to pander to ignorance and fears about the future of content distribution to end users. Such fear and ignorance is a cornerstone of ill-fated decisions made in haste and lacking proper scrutiny. After all, isn’t the real challenge of content providers today and into the future to deliver content to all consumer devices, not just TV's in the home? TV’s now stand in the company of smart phones, lap tops and tablets. It’s a fact, and our children and grandchildren prove it every day, that our lives today and tomorrow revolve around our ability to access content Anywhere, Any time, and via Any device. This ability should be hallmarks by which we consumers measure a provider’s capability and value.

So allow me to respond to the statements made in this section of your letter:

1. "Our current TV service is provided ... through a coaxial cable system which was installed at the time WT was built over 20 years ago."

A statement like this infers that the system built then has never been maintained, repaired or upgraded. That the cable is "old" and thus cannot accommodate today's demands for data and content.

Fact: Over the years, Comcast has operated a robust and technically superior cable system as required by its cable franchise and FCC specifications. It is NOT a coax only system. It is a Hybrid Fiber Coax (HFC) system containing both Fiber and Coax. AS for WT, the many Fiber Nodes within WT are engineered to scale signal and data capacity many times over. Over the years, the coax segments under our streets and through our neighborhoods (spans) have been replaced, repaired and/or upgraded as needed to ensure delivery of the full portfolio of Comcast services offered. Yes that includes High Definition TV on all TV’s throughout the house, Telephone service, Home Security, and the fastest Internet available. Here's a fact not to ignore: Comcast currently has almost 80% of WT homes as Internet subscribers. Yes, that means well over 1500 homes in WT are COMCAST Internet subscribers…all delivered via Comcast’s HFC system. How could it be that Comcast’s facilities are old and “obsolete” when so many of our neighbors are being served today the broad array of advanced products and services?

2. "This technology (Coax) has been around for over 30 years, is obsolete and has no room for expansion or upgrading. The Coaxial signal is shared by all users…"

Fact: Coax delivers with no problem any and all broadband services today and WELL into the future. COAX IS NOT OBSOLETE!!! It is a highly capable medium to technically serve as a backbone of many company and government networks. Coax is still widely relied upon, in conjunction with fiber, to serve the bandwidth needs of our society. Also, the signals delivered to each household in WT are NOT shared. Each house, depending on its cable subscriptions, is provisioned with the required bandwidth to deliver its subscribed services. One household’s use is exclusive and independent of its neighbors.

3. “Fiber Optic technology is the latest and greatest…”

Fact: Fiber has served major network carriers, including Comcast, for at least 25 years along with coaxial and other copper mediums to connect end users reliably and efficiently. Most Service Provider network back bones are fiber driven and while the recent trend is for providers is to extend fiber connections closer to end user devices (i.e. TV’s, Computers, Telephone), quality of service is still in large part contingent on the medium it connects to (inside home wiring). As the saying goes, “only as strong as the weakest link.” As for Cat 5E cabling, which is nothing more than copper telephone wire, is no better than coax cabling that connects fiber to end user devices.

Facts about Comcast’s proposal to Winston Trails.

Comcast HAS made it clear to the Cable Committee,” if fiber is what you want then we’ll build it”. However, the committee expressed their concern about likely disruptions due to property wreck out and the laying of cabling across the community. At the time, the Committee informed Comcast that they would be favorable to a proposal for upgraded services without fiber. However, since then, the Committee sought no additional proposal from Comcast for Fiber to the Home (FTTH) configuration and went silent on requests for additional information.

FACT: In the past two years, Comcast have converted large scale communities to FTTH. All new build communities are now being built with Fiber exclusively. Existing communities are regularly being reviewed for fiber upgrades. WT is one that Comcast has agreed to UPGRADE>

What to Consider:

Comcast current Bulk Agreement expires April 2017. Twenty Two months remaining.

Comcast will continue to advance and scale its product line (increasing internet speeds, X1 Video Platform – Emmy Award Winner). Subscribers will have complete choice of service type and level. Not so with Hotwire.

Comcast is THE largest Internet Service Provider (ISP) in the country. Carrier Class network and leading edge service platform provides the FASTEST internet and Award Winning Video. Comcast OWNS favorite cable channels and the entire library of content from Universal Studios. Hotwire uses multiple networks for its internet service and is a member of a satellite consortium to resell satellite Video programming. It owns ZERO content.

Comcast is willing to continue to be the bulk provider of choice in any capacity the community desires as follows:

VIDEO ONLY - continue to serve WT with Basic Digital Video. Keep rate as low as possible. Negotiate short term. Hotwire does not deliver video only. They MUST HAVE multiple services committed to for LONG TERM – TEN YEARS

DOUBLE PLAY – Upgrade Video to X1 Video Platform. Add High Speed Internet service. Competitive pricing and terms vs Hotwire.

Finally, if WT chooses to not bulk with any provider, please know Comcast will continue to provide all its services to residents with promotional offers as it does with thousands of communities across the nation. Comcast will gladly compete with ANY available provider household by household. Hot wire will NOT build out a network to compete. They want a guaranteed customer base loaded up with multiple services!!!

DON’T let the Cable Committee (two people) decide for you.!!!! You have a say as a WT Homeowner and member of the Association. Let them know you wish to stay with a provider that is an industry leader, abundant with service options and price bundles, proven long term reliability, Disaster recover expertise, along with award winning products and services. Please let your thoughts and opinions be heard at the Tue June 9th meeting. See you there.

Best Wishes

Vince Friscia

Speechless: The Kardashian’s are now house flippers

“No more neighbors, friends whose past Real Estate experience is renting an apartment or buying a starter house, or stay-at-home moms flipping houses locally; young, flamboyant Realtors on reality, cable TV shows selling multi-million dollar trophy properties to those from abroad with briefcases of cash that until this year bought a lot relative to the ‘weak’ US dollar; 20-something Silicon-kids paying $2,000/sq ft for a house they could buy 20 miles away for $500; large, institutional private equity firms buying 10s of thousands of single-family houses for rental purposes — sight unseens using computer programs — thinking a 3% yield is acceptable long-term and somehow, someday economies of scale will emerge; or individual / “family-style” speculators committing lending fraud at a pace that rivals 2006 chasing their share of the “easy money” in Real Estate, are needed to prove to me that Bubble 2.0 is not just a monster, greater in intensity and energy than Bubble 1.0, but will end the very same way…”

The above is just the opening paragraph for a great post by Mark Hanson…take the time to read the entire (not too long, but extremely important) post here!

If you own a home and are thinking about selling in the near future…you have to read this.

If you are considering getting in on the new ‘HGTV flipping’ craze…you have to read this.

Even if you are a ‘buy and hold’ investor…you have to read this.

Thanks for reading my blog!

Steve Jackson, 561 602 1258